"Unprecedented Chaos"!

An expected 4-Day war is turning out to be a “Historic Mess” in the Middle East, which is “hours” away from rattling the global trade and financial markets.

We saw an unprecedented price action in oil this week.

Producers rushing to hedge (hedging demand), a historic short squeeze, and speculative frenzy (USO witnessed the biggest day of retail net buying yesterday) led to a historic week, with Crude futures posting the biggest weekly jump since 1985, rising 34%.

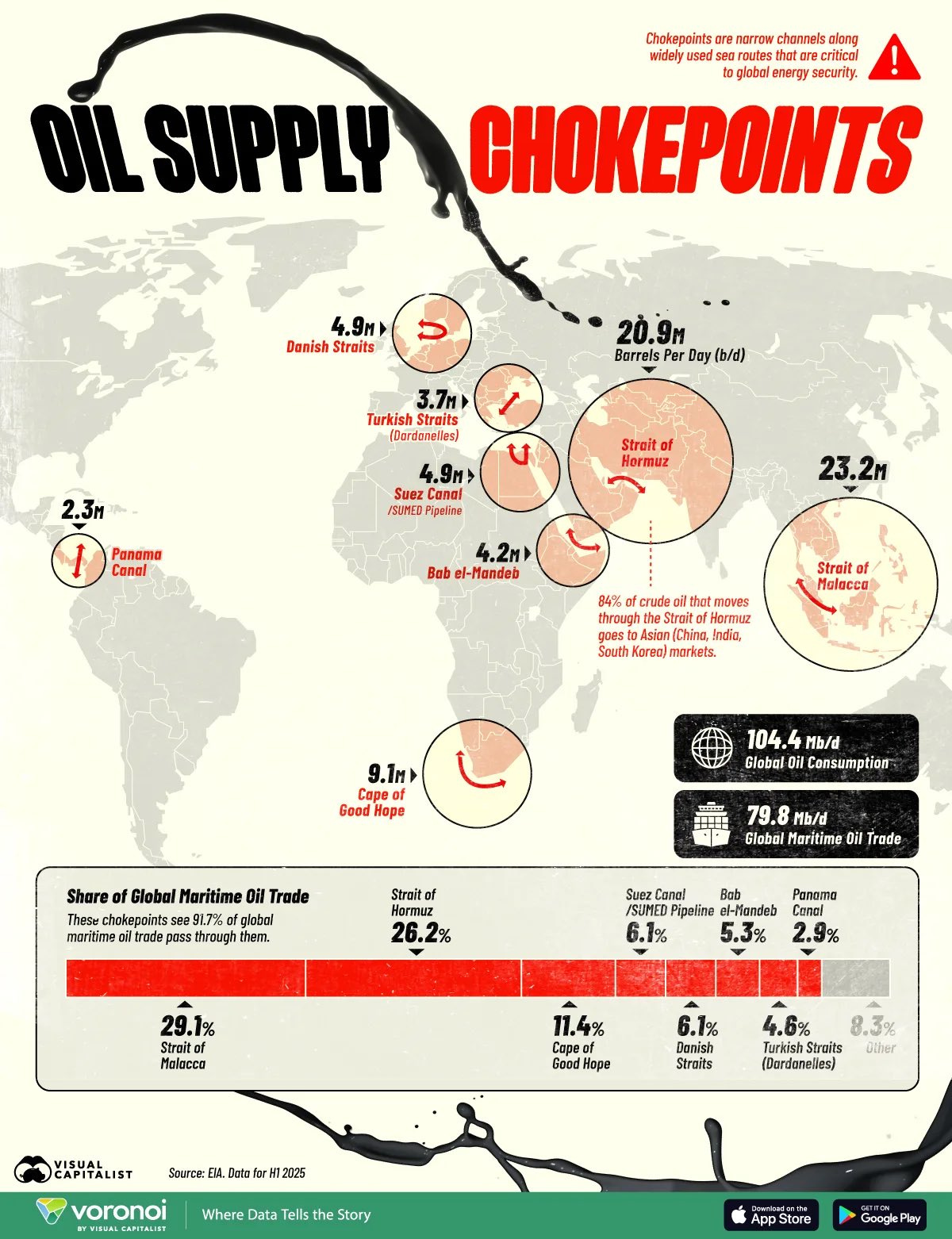

Whenever the Iran-US/Israel war was discussed in the past, the worst-case scenario involved the closure of the Strait of Hormuz.

For those who are unaware of the significance of the Strait of Hormuz, let us explain to you:

More than 20 mbpd of crude flows through the Strait of Hormuz, roughly 20% of total world oil consumption (per day).

Furthermore, 84% of the crude from the Strait goes to only three countries: China, India and South Korea.

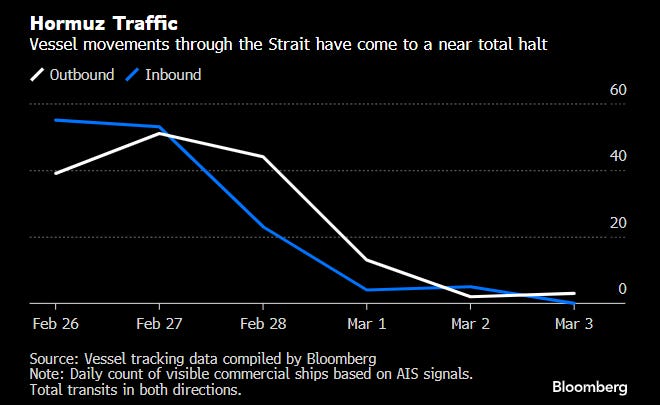

In the last week, Hormuz traffic has come to a complete halt.

This implies that we just witnessed one of the biggest disruptions in history.

Today, we will discuss the consequences of the disruption and model different scenarios and the likely cross-asset movements. (Paid subscribers can directly jump to the geopolitical section for war/oil analysis.)

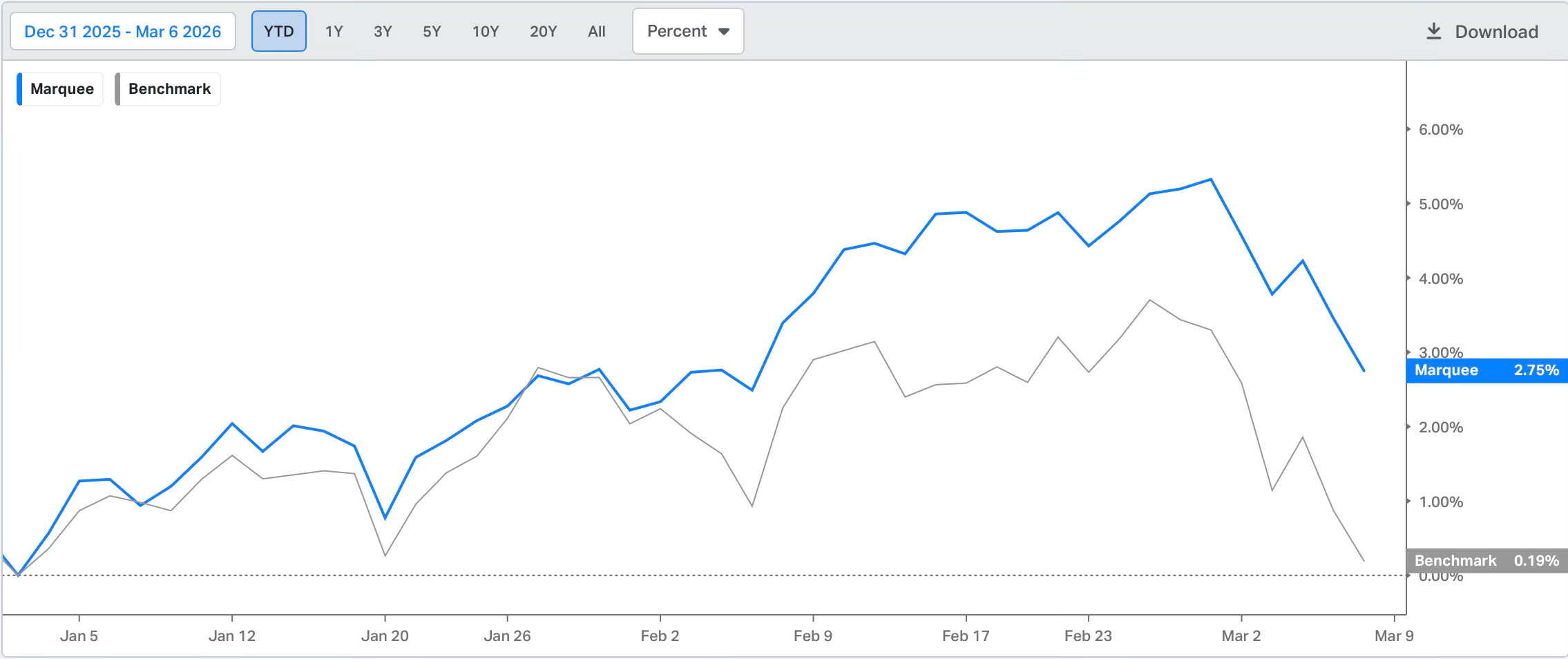

Despite an extremely volatile environment, we continue to outperform the benchmark by more than 250 bps.

US/Equities/Bonds/Oil/Gold/Silver/Dollar!

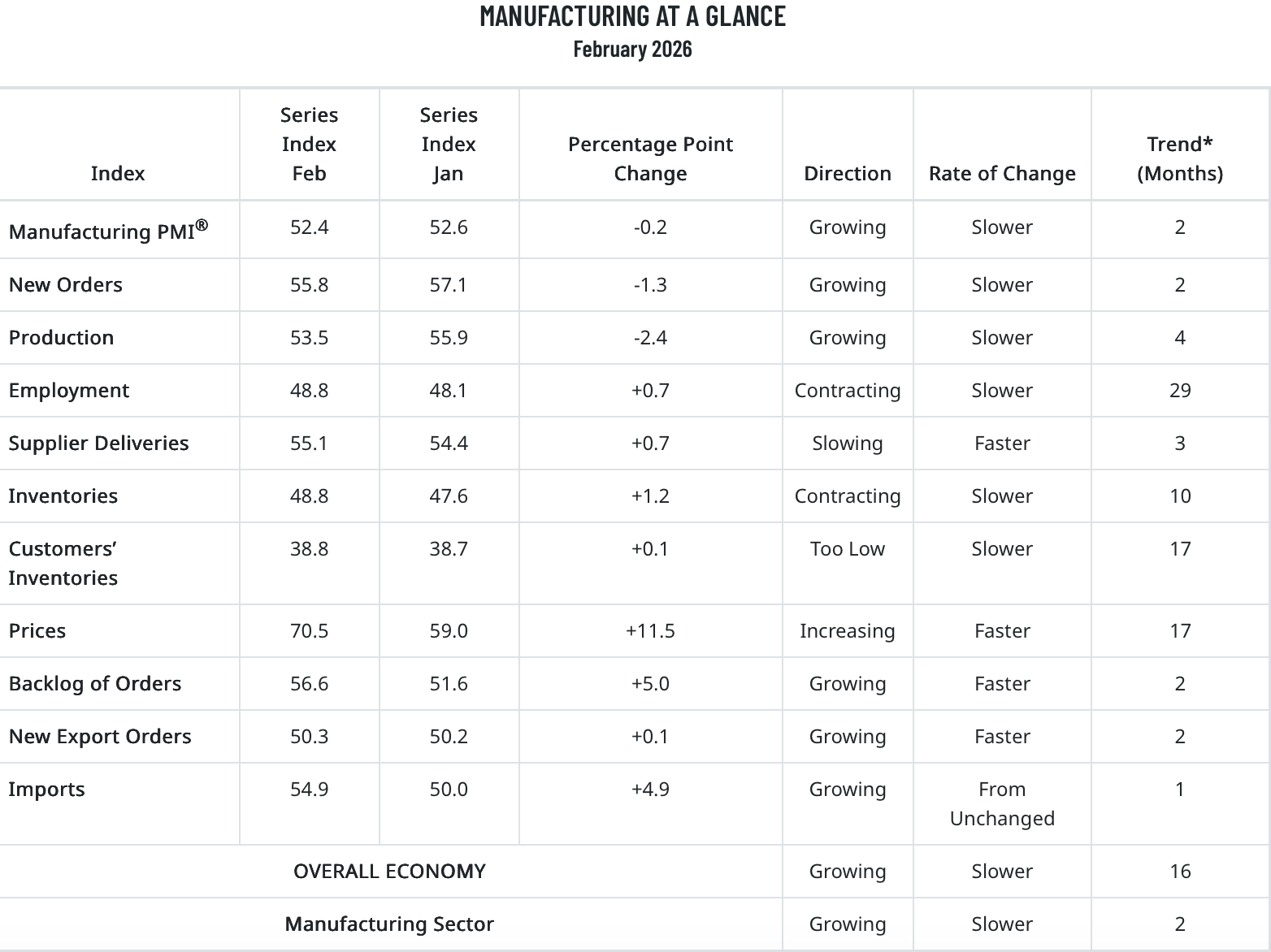

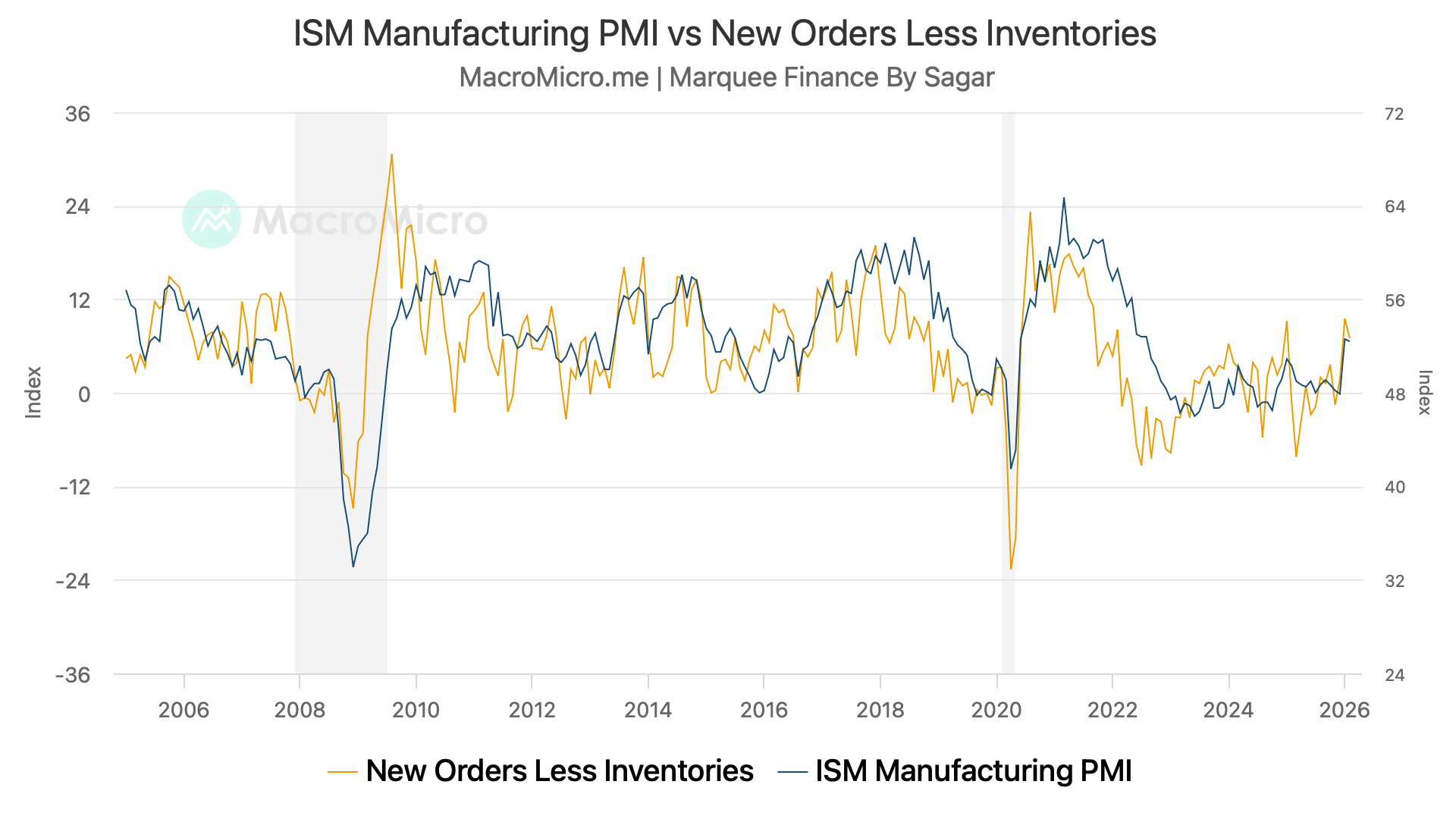

Our favourite indicator of the cyclical economy has been the ISM Manufacturing Index.

Note that since 2022, ISM Manufacturing has been in a contraction zone as “manufacturing” and housing were in a recession.

However, since the last two months, there has been a notable recovery in the ISM Manufacturing.

We are now in an expansionary zone (greater than 50) with all the sub-components reporting satisfactory growth (except Employment, which is still below 50: contraction, but has been trending up).

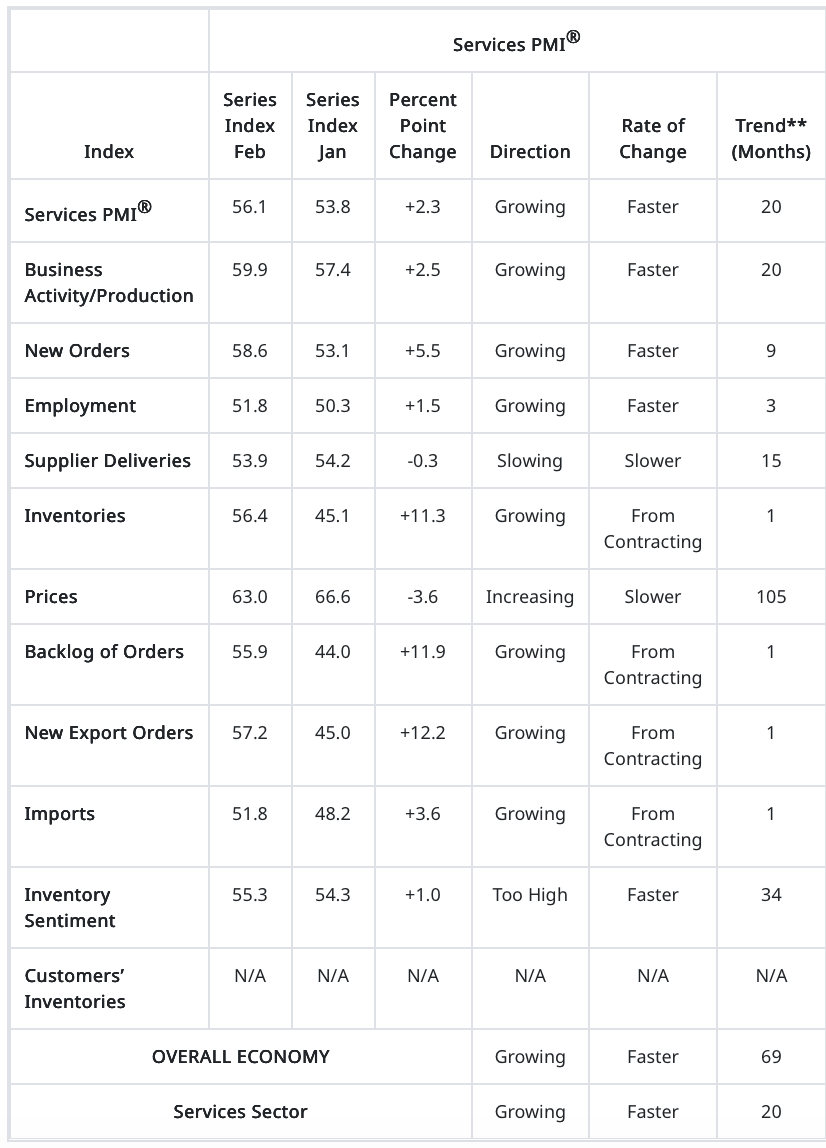

However, when we dig deeper, the worrying signal is the ISM Manufacturing Prices Paid, which came in scorching hot at 70.5.

With oil prices on a tear, we don’t expect it to fall anytime soon, which will lead to higher prices for manufactured products in the coming months.

Our leading indicator for ISM Manufacturing is New Orders Less Inventories, which is buoyant and suggests that the manufacturing recovery will continue unabated.

ISM Services also came in higher than expected (the highest since 2022), with most subcomponents reporting robust growth.

The encouraging part was also the ISM Services Prices Paid, which fell MoM, and the trend seems to be lower (might change with elevated oil prices).

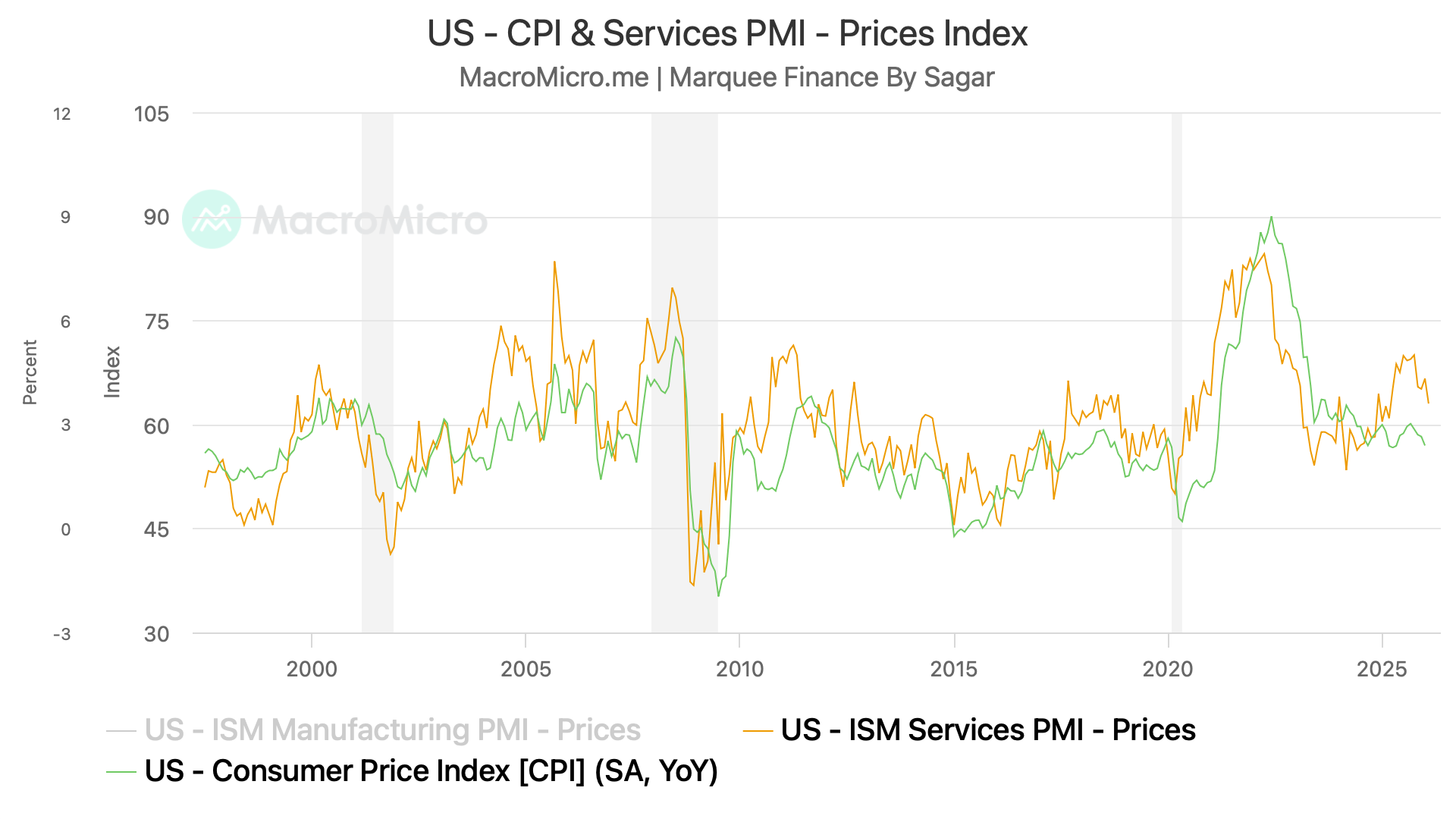

We discussed last month that with ISM Services Prices peaking, we might have seen a peak in the CPI due to the tight correlation between the two series.

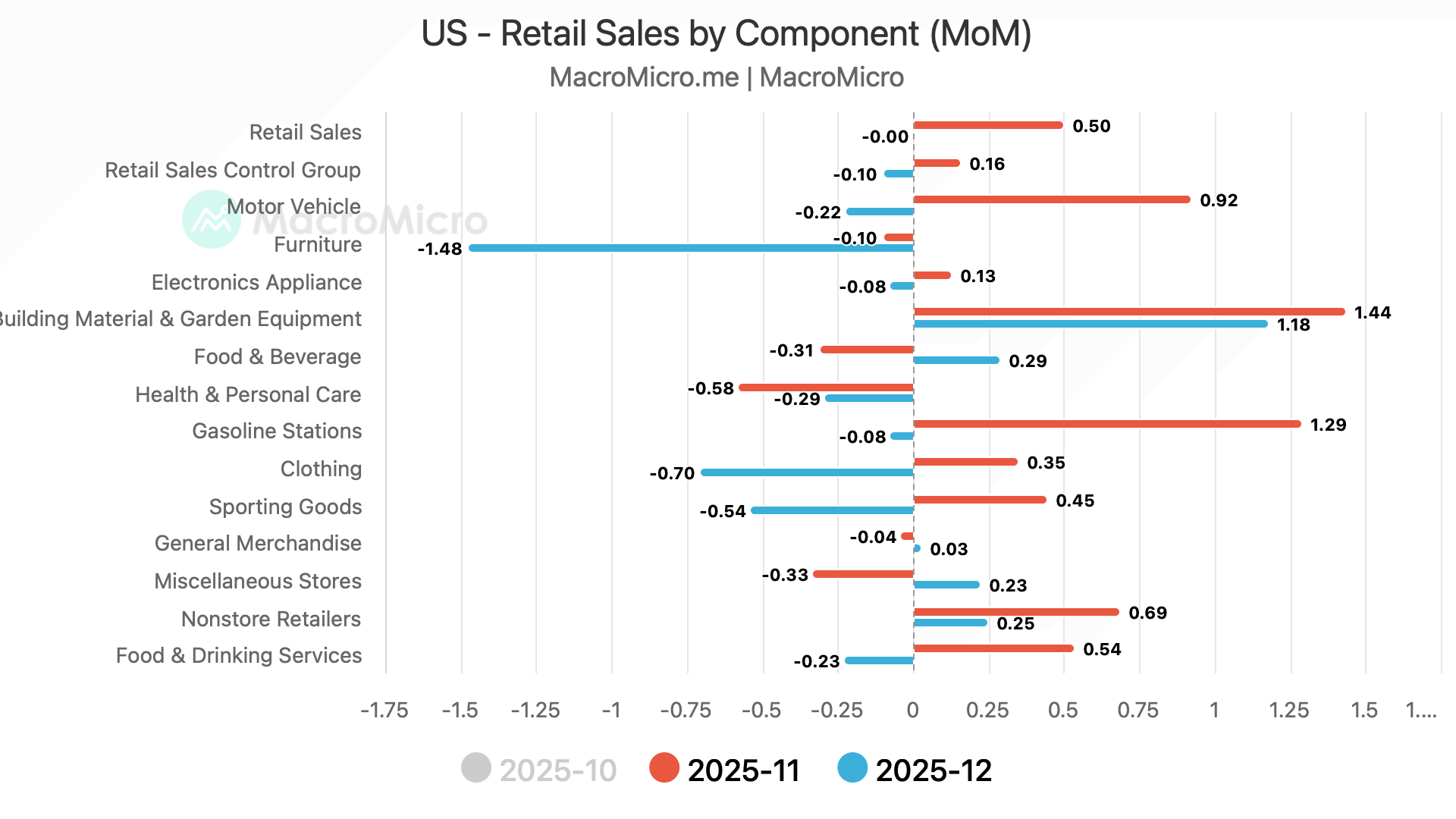

Retail Sales came in slightly better than estimates.

Headline Retail Sales -0.2%, Exp. -0.3%

Retail Sales ex auto 0.0%, Exp. 0.0%

Retail Sales Control Group 0.3%, Exp. 0.3%

However, the housing-related components are still weak.

We expect retail sales to moderate further if oil prices remain above $80-90 for a prolonged period, as this will squeeze American households, given that real incomes have been declining for more than a year now.

Now let’s jump to the macro shocker of the week: