Weekly Update!

US/Equities/Bonds/Gold/Oil/Dollar!

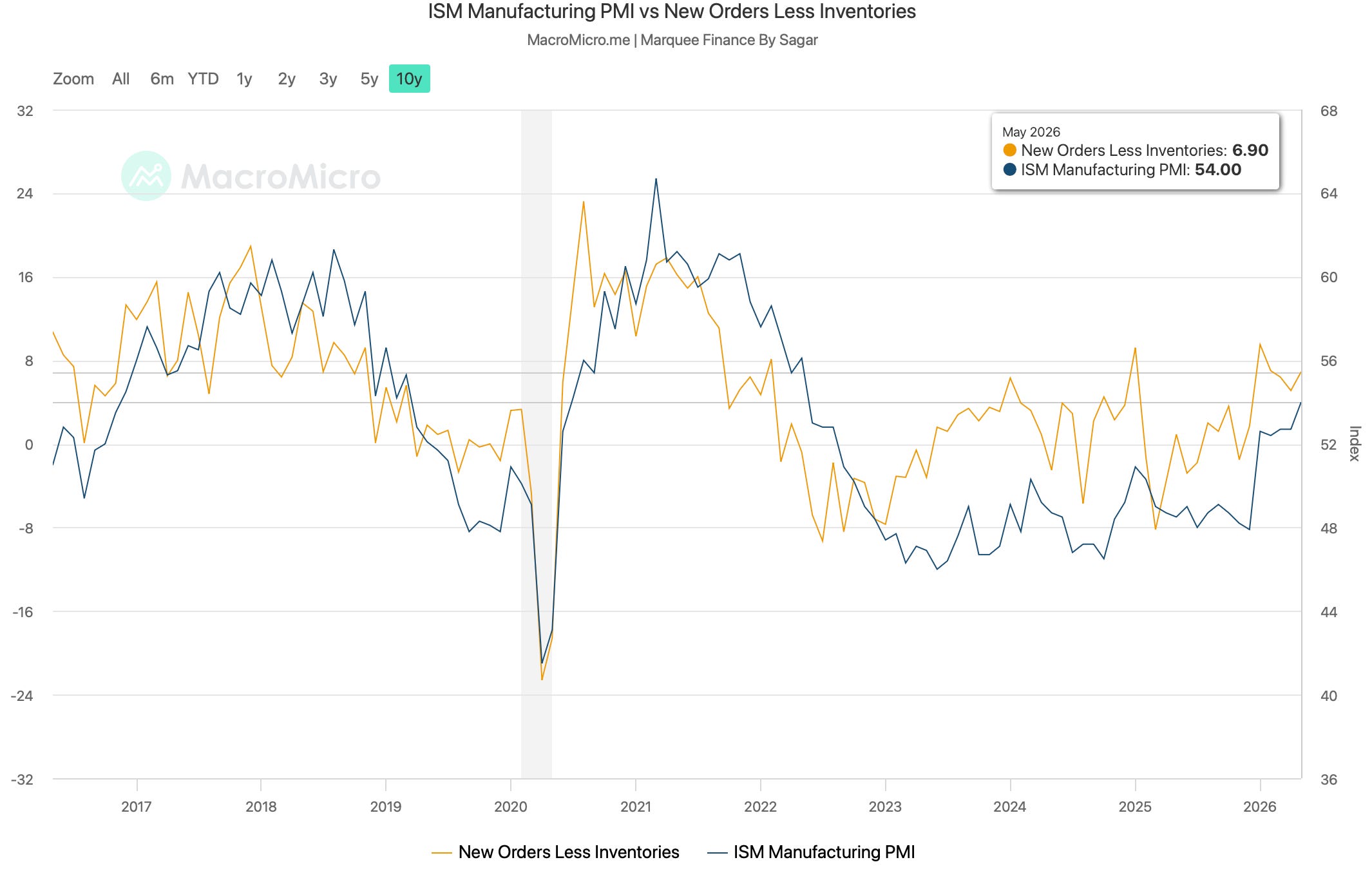

Long-time readers know that ISM Manufacturing is our preferred indicator for tracking US cyclical activity.

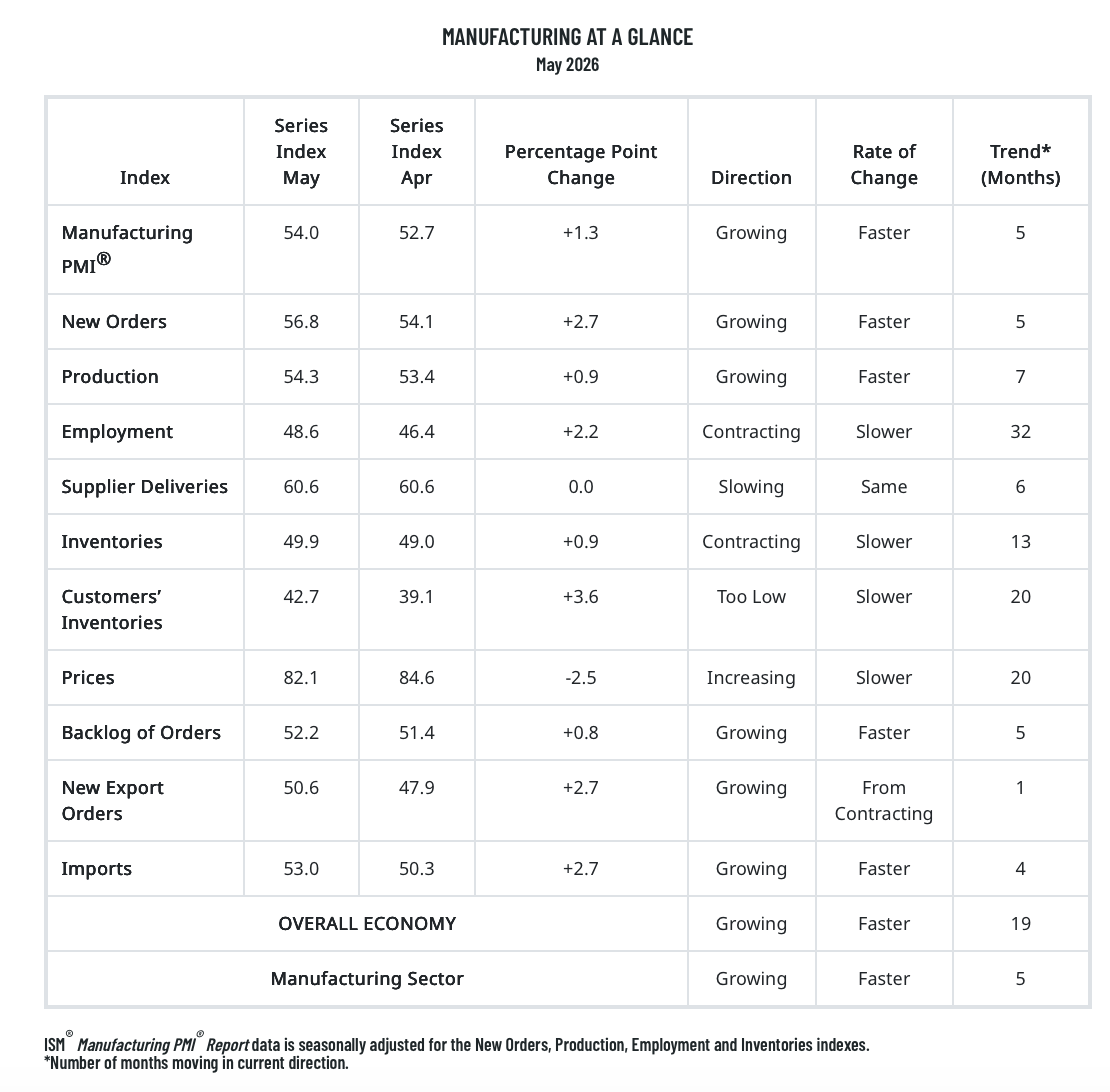

The ISM Manufacturing came in at 54, indicating significant expansion. In fact, the number was the highest since May 2022.

Furthermore, New Orders Less Inventories is once again moving higher, indicating that we might see continued acceleration in the cyclical activity thanks to the enormous AI spending by hyperscalers.

The internals of the ISM Manufacturing demonstrate a broad-based expansion (>50) across sub-components.

However, the Prices PMI is running extremely hot, so expect CPI to flare up.

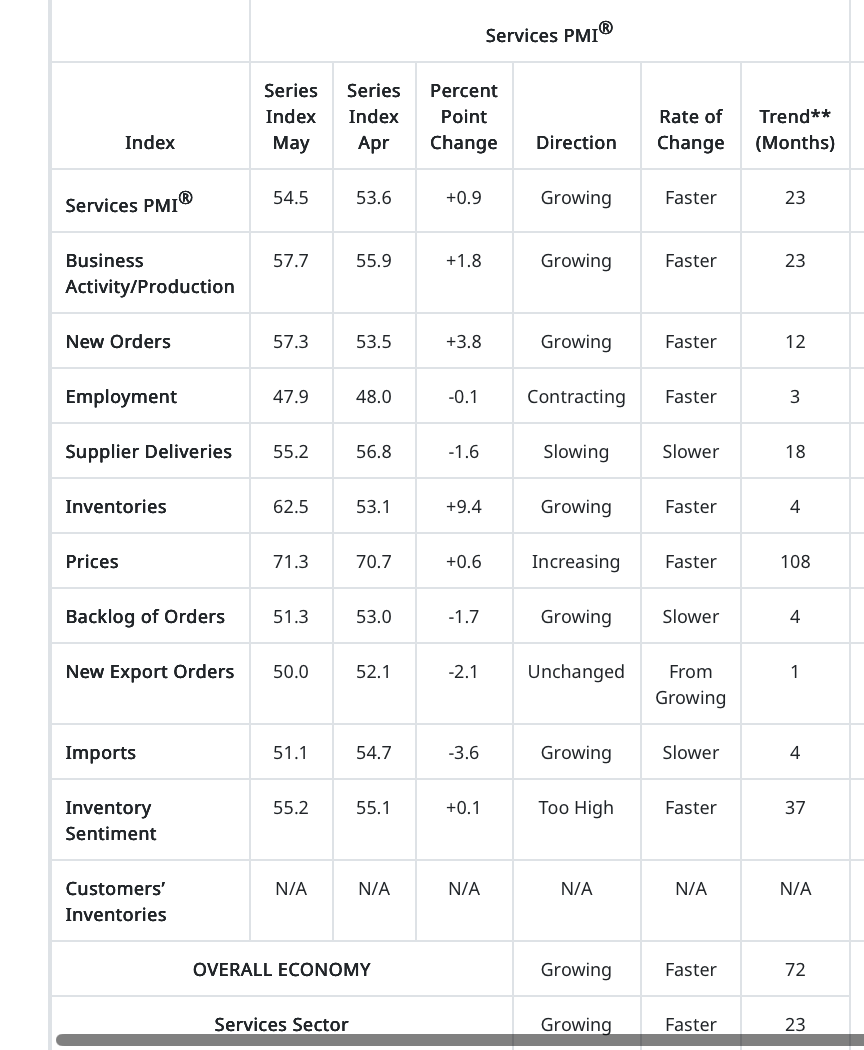

ISM Services came in strong at 54.5 v/s expected 53.8. While New Orders were strong at 57.3, a rise in inventories is a concern.

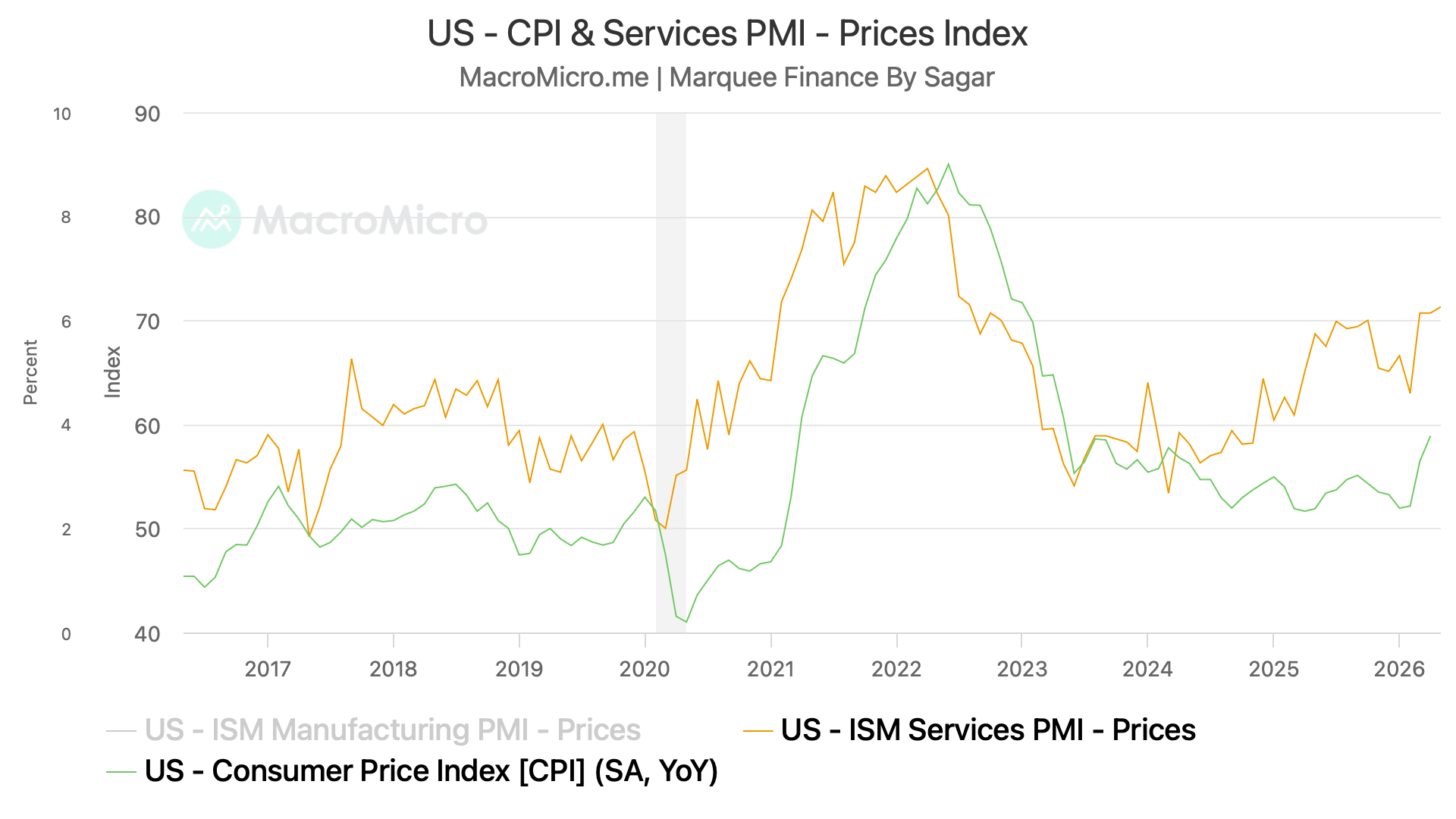

ISM Services Prices have a high correlation with the US CPI.

ISM Services prices continue to rise gradually, and thus, we expect the CPI will follow suit.

Note that the CPI is a lagging indicator, and a higher CPI will be visible with a 2-3-quarter lag.

Let us now analyse the labour market data:

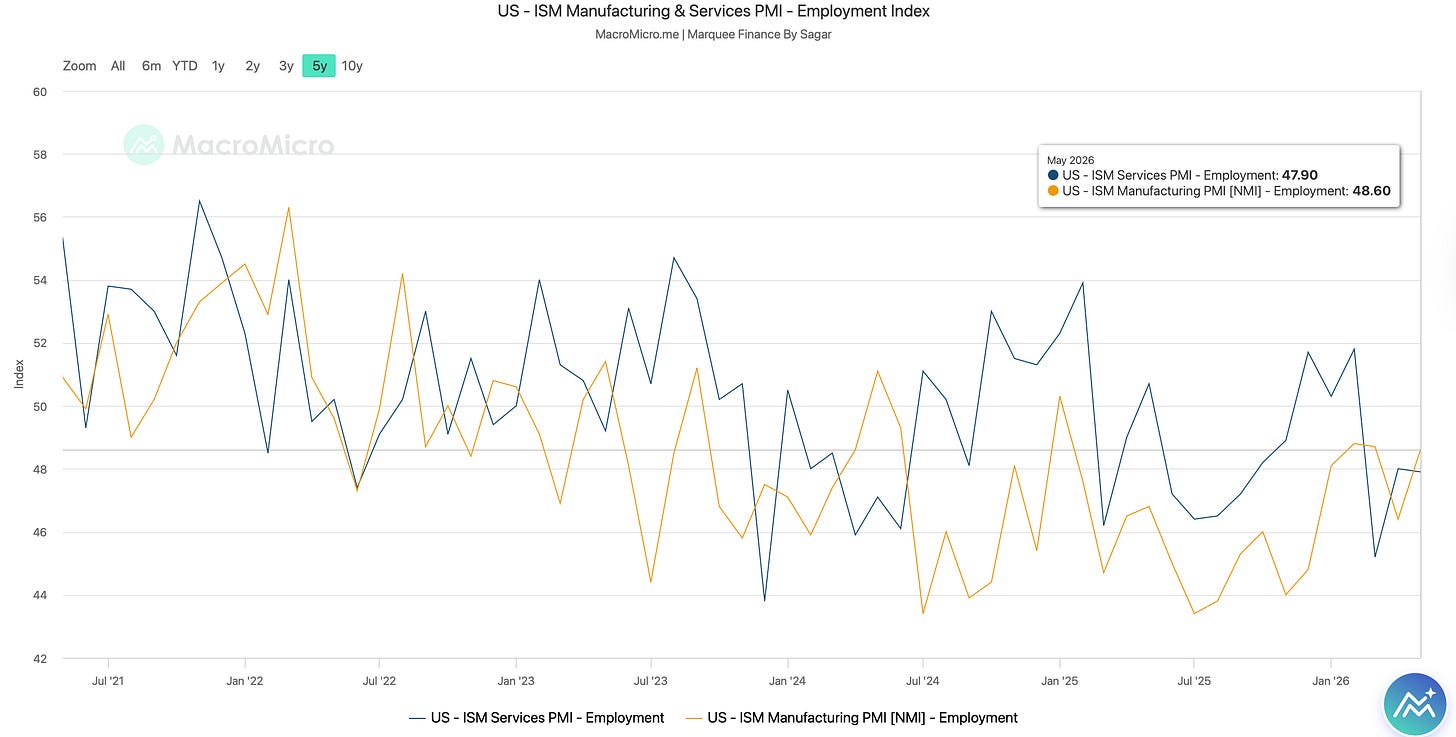

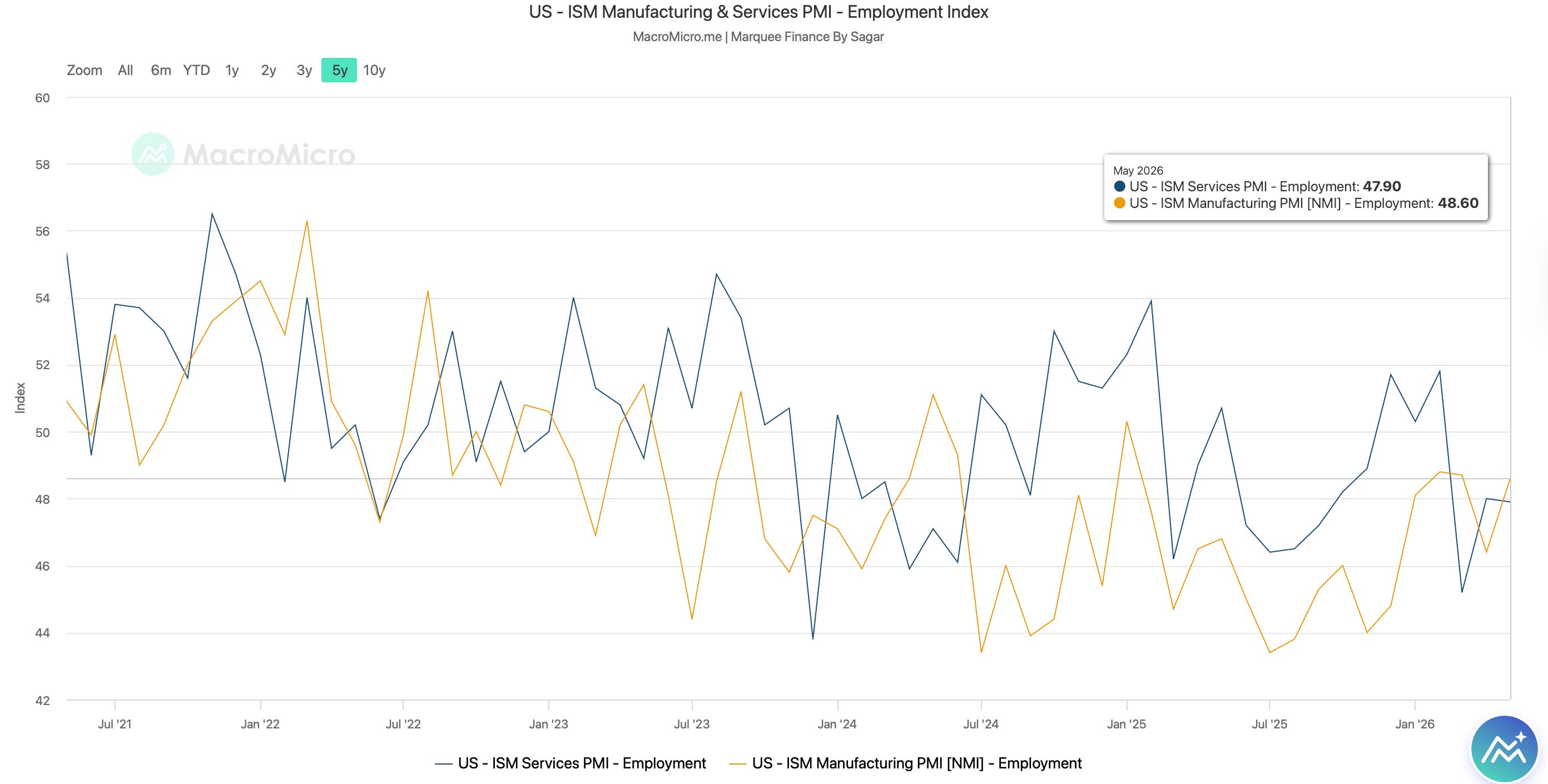

ISM Manufacturing and Services Employment: Although ISM Manufacturing Employment PMI is still in contractionary territory (<50), it is on the verge of moving higher to expansionary territory (>50). Note that the last time it was higher than 50 was in January 2025. ISM Services PMI remains subdued (this is due to layoffs in the financial services sector, driven by AI).

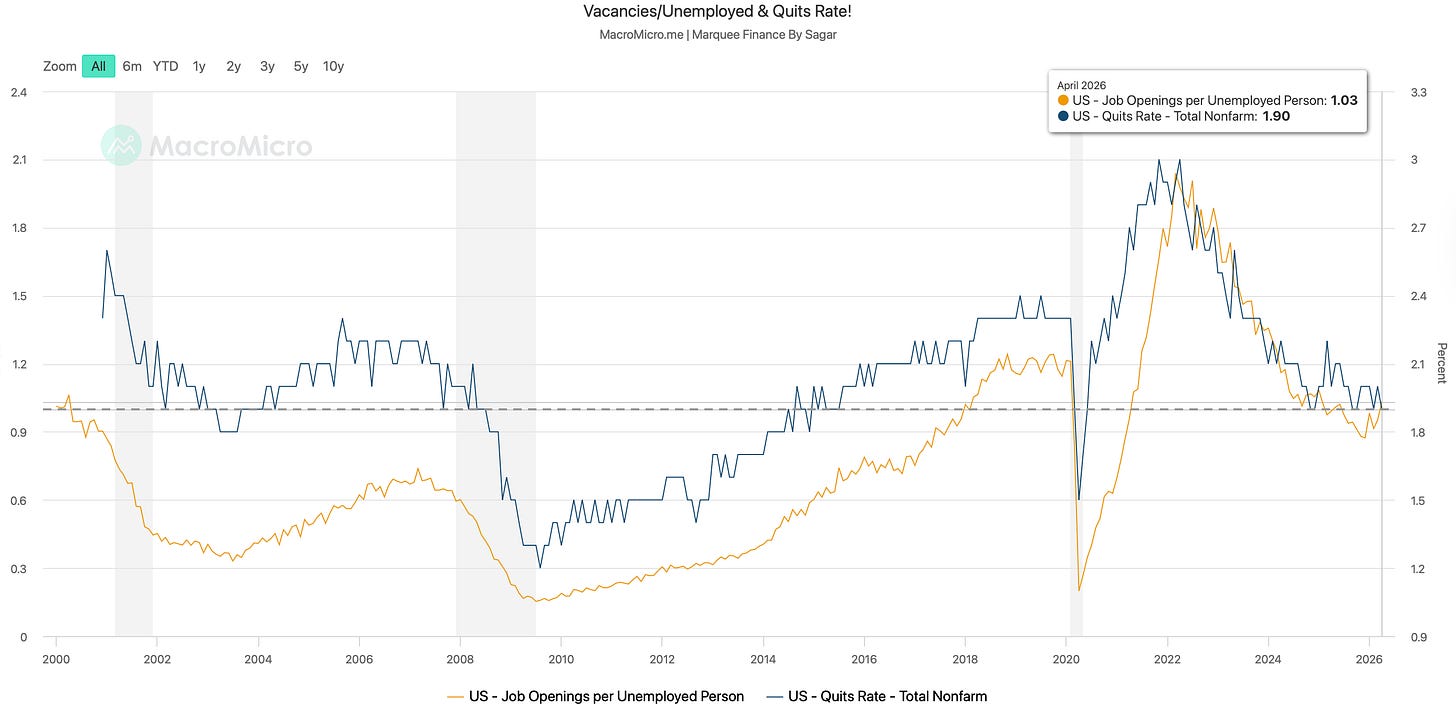

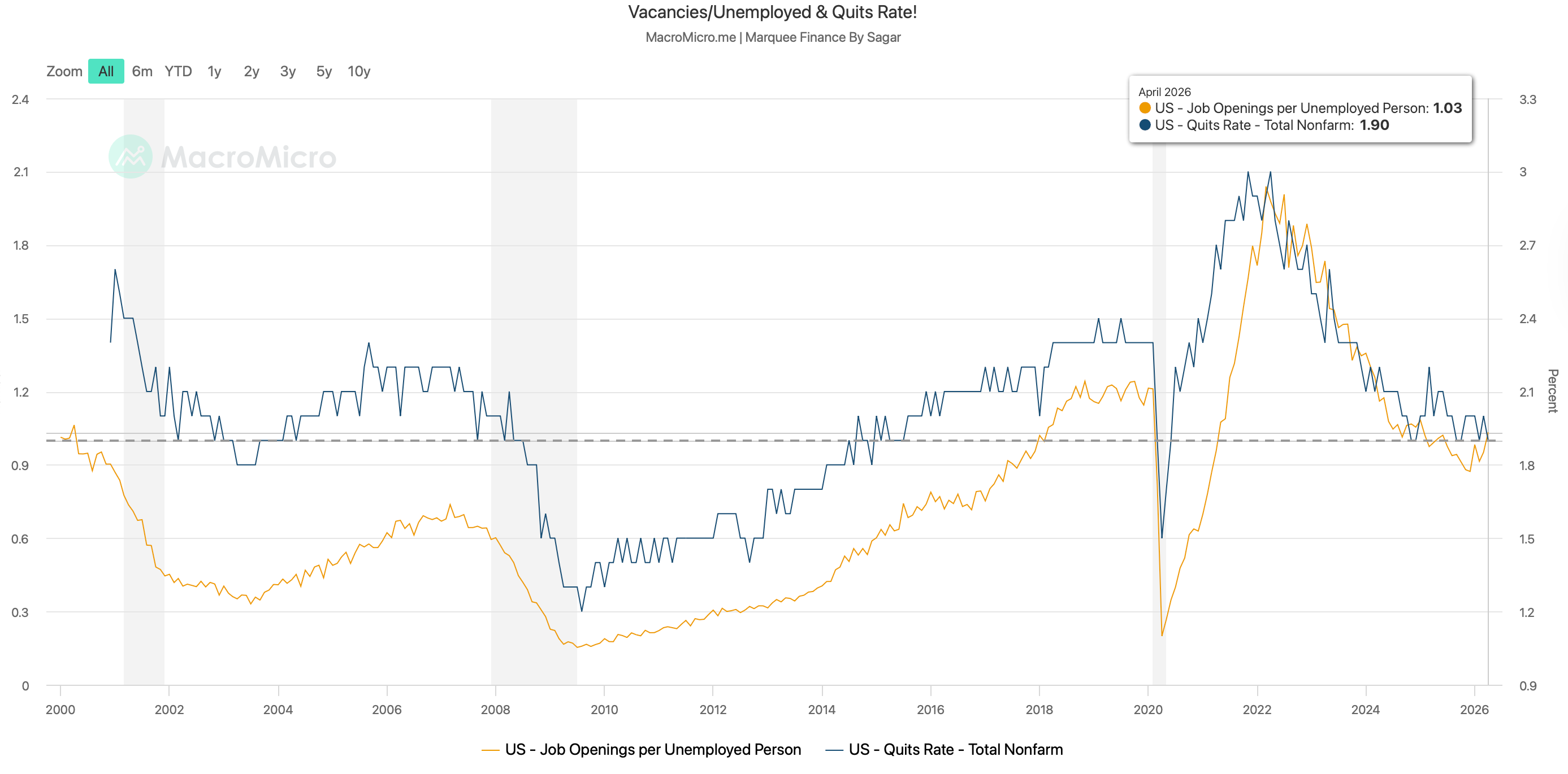

JOLTS-1: Fed’s preferred gauge to track the labour market is the Vacancies/Unemployment Ratio, which bottomed out a few months ago. In fact, we are now at 1.03, well above the lows of 0.87. On the other hand, as a result of the no-hire, no-fire regime, the Quits Rate has once again plunged to the multi-year lows of 1.9%.

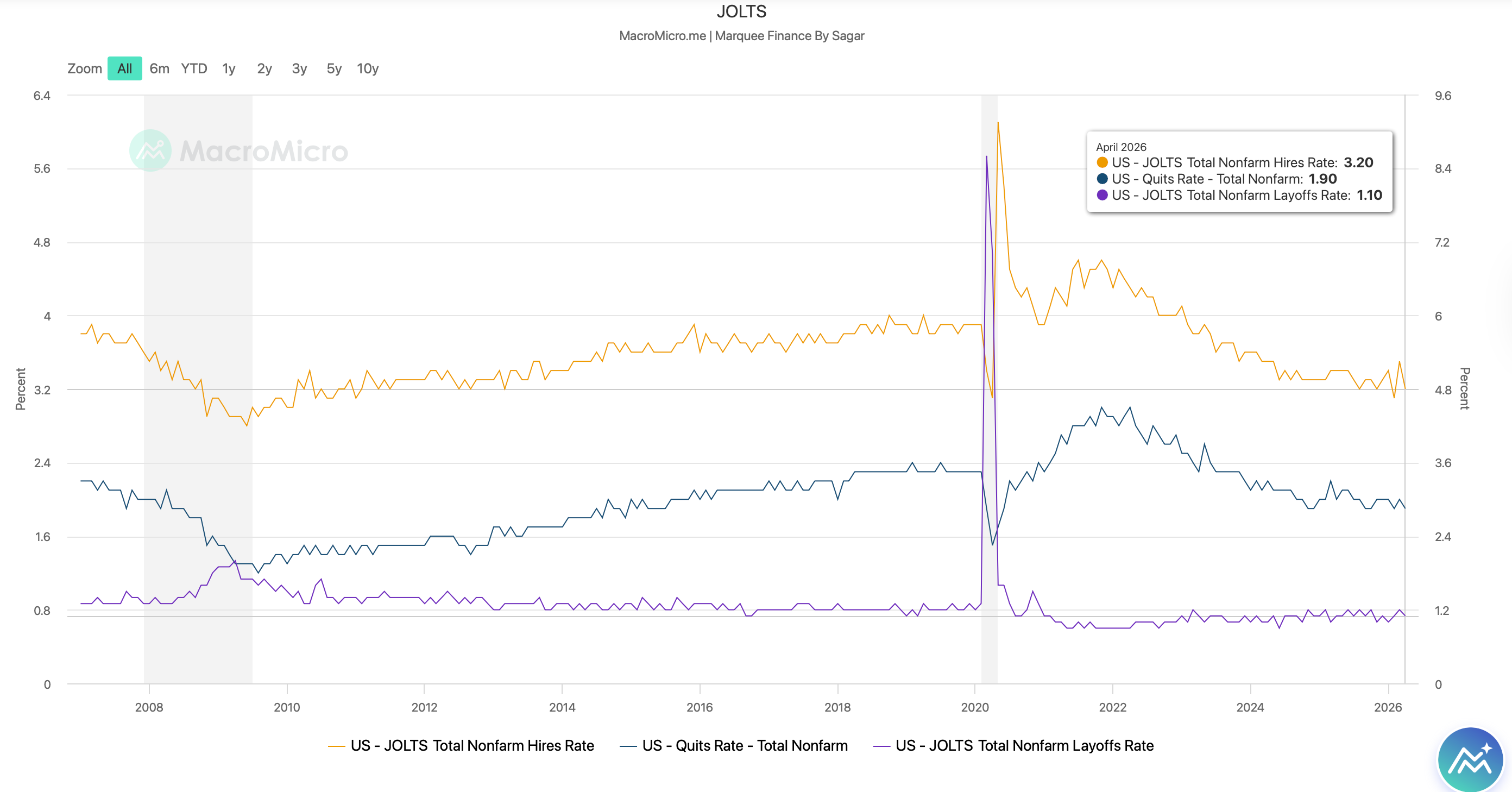

JOLTS-2: While the Quits Rate is back at lows, the Hires Rate, which bumped up higher once again, fell to 3.2%, although still 10 bps above lows. The layoff rate also fell 10 bps to 1.10%. No hire, no fire regime prevails in the US.

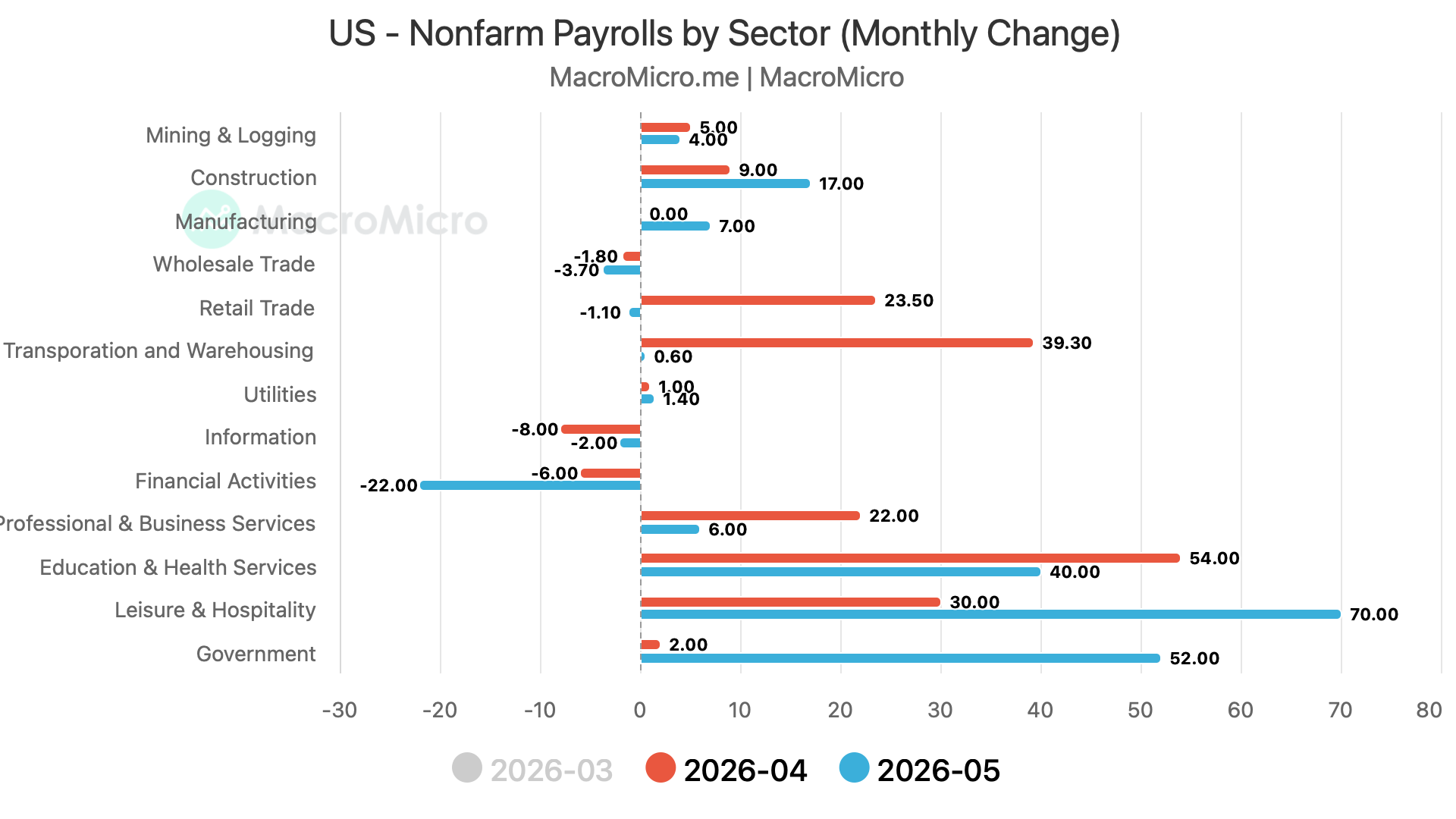

Non-Farm Payrolls: The US economy added 172k jobs, a massive beat against expectations of 87k. There were multiple tailwinds (the Memorial Day holiday effect, FIFA World Cup hiring, etc.) that led to the enormous surprise. Furthermore, the Government Sector hiring once again picked up. Note that since the last few months, we have seen subdued government hiring post mass layoffs. Leisure and hospitality saw a massive bump due to the FIFA World Cup.

NFP Internals: While over the last two months we saw considerable improvement in the labour market, as measured by Part-Time Economic Reason and Full-Time Employment as % of Labour Force, this month there was a slight deterioration despite positive revisions and a beat on the headline number.