A Historic Regime Change?

“My colleagues over the last two days, and frankly, the first three weeks I’ve been here, they’ve been very open about changes. Change isn’t easy; change is filled with risk.”- Kevin Warsh, 17th October 2026.

We might be on the cusp of a historic regime change at the world’s largest central bank.

If Kevin Warsh executes on what he promised at his first-ever FOMC, the way we process macro data and the way the market reacts to the Fed & the incoming macro data will undergo a sea change.

In fact, not only will the macro framework at Marquee Finance By Sagar will be tweaked, but the entire category of macro hedge funds will have to replace their macro models to fit in the new regime.

We will later discuss in detail the FOMC overhaul planned by Warsh.

As the “Treaty of Versailles” was signed by both the US and Iranian Presidents, with details emerging in bits and pieces, the event will be remembered in the history books forever.

For us, unsurprisingly, a new regional power has emerged post-war, with far-reaching consequences.

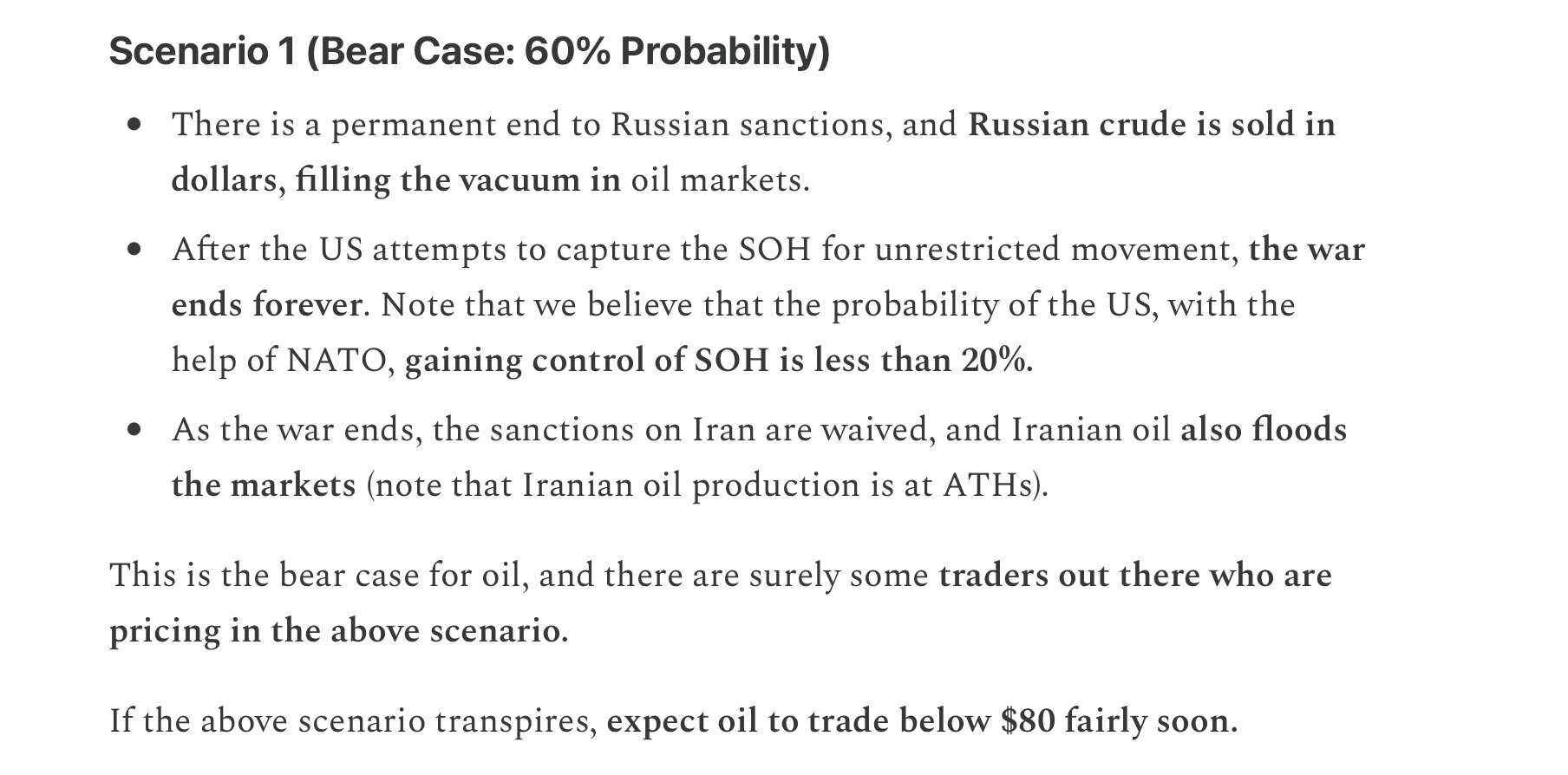

On 11th April, in “Million Dollar Question”, we mentioned the following to our paid subscribers:

Although we were wrong about the ground invasion, we got the oil below $80 correct. This was at a time when oil was oscillating above $100, and the calls were out for $200.

Since the beginning of the war, we have only twice been wrong about the direction of cross-asset markets.

Once, at the beginning, when we thought that the war would be over within days (due to low ammunition, etc.).

Second, when we thought the ceasefire would not hold, and we would get a ground invasion.

Note that we correctly predicted the moves in the bond markets. Even bought bonds (duration) at the bottom twice.

However, around 16th-17th April, we became confident in the upmove in the equity markets and positioned accordingly.

Nevertheless, we still underperformed.

Reason?

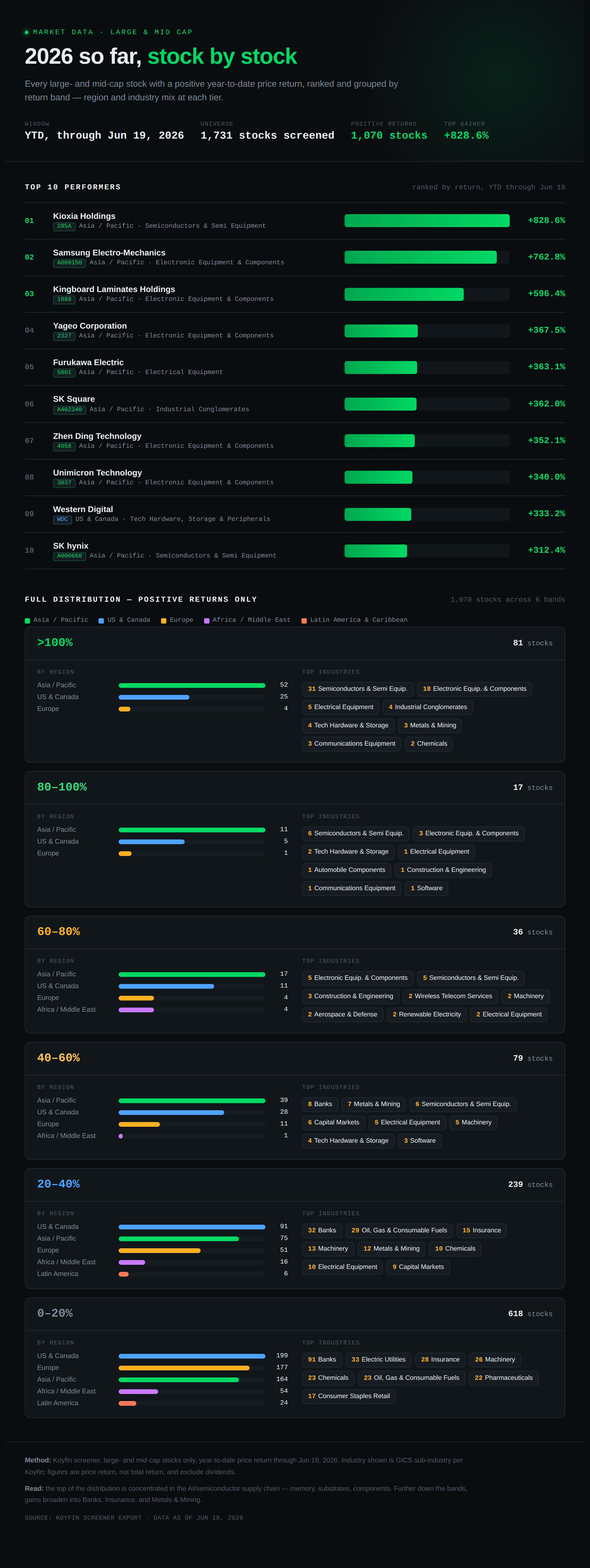

Check this chart we prepared using Claude (data from Koyfin)!

More than 135 stocks are up >60% in the MSCI ACWI Index since the beginning of the year, and no prizes for guessing: more than 80 of them are semis/hardware.

In fact, the list contains the top 10 stocks by return, and all are semiconductors/hardware (mostly in Korea/Japan).

The portfolio is slightly down this month; however, it is near YTD highs (the first column shows annual returns/YTD, followed by monthly returns).

The Chinese equities have been a major drag on the PF with roughly 80-90 bps of underperformance attributed to China.

However, we remain confident and are in a wait-and-watch mode on China.

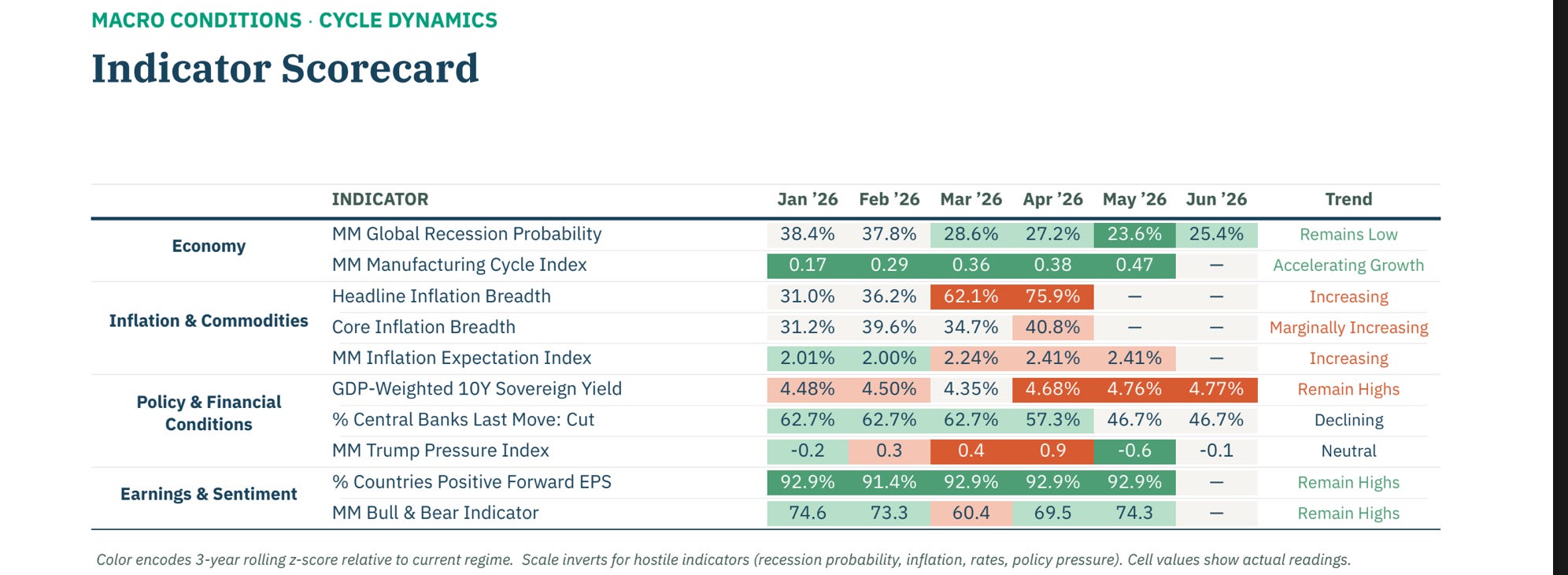

PS: We are in the process of building a high-quality macro dashboard. Using AI, we are automating the framework and indicators we use for asset allocation.

MacroMicro uses a “very” simple dashboard to track the cycle.

We will further “significantly” enhance the dashboard using our indicators and, as usual, join the dots.

The “GLOBAL” Macro Dashboard will be an expensive product ($1000+ One time), and the paid subscribers will get a significant discount. It might take weeks to unveil it as a lot of work will go into it with extensive backtesting. Note that it will also use technical analysis as a supplement to recommed the asset allocation.

Let’s do a deep dive into the macro universe and comprehend the cross-asset moves.

US/Equities/Bonds/Dollar/Oil/Gold!

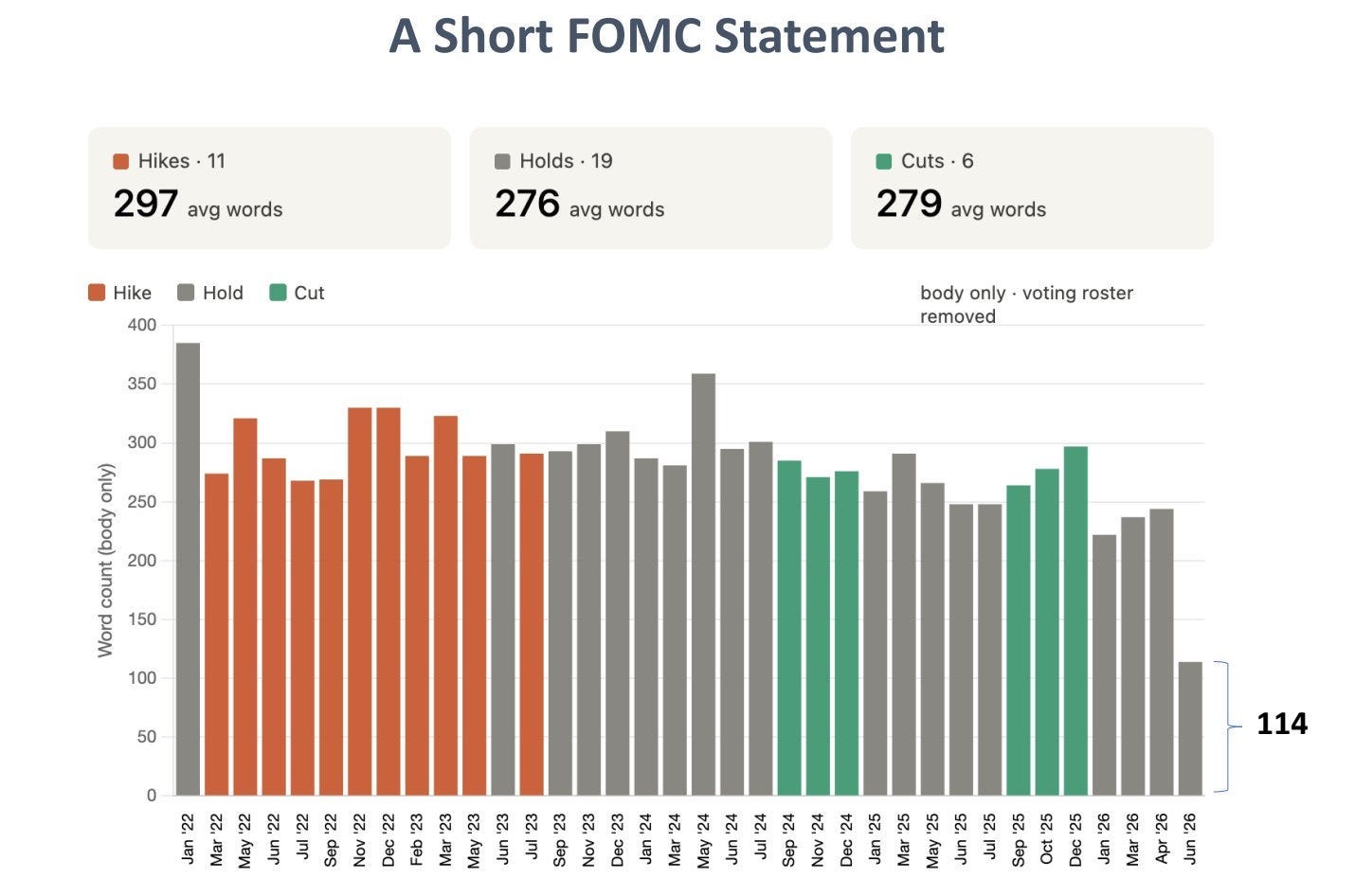

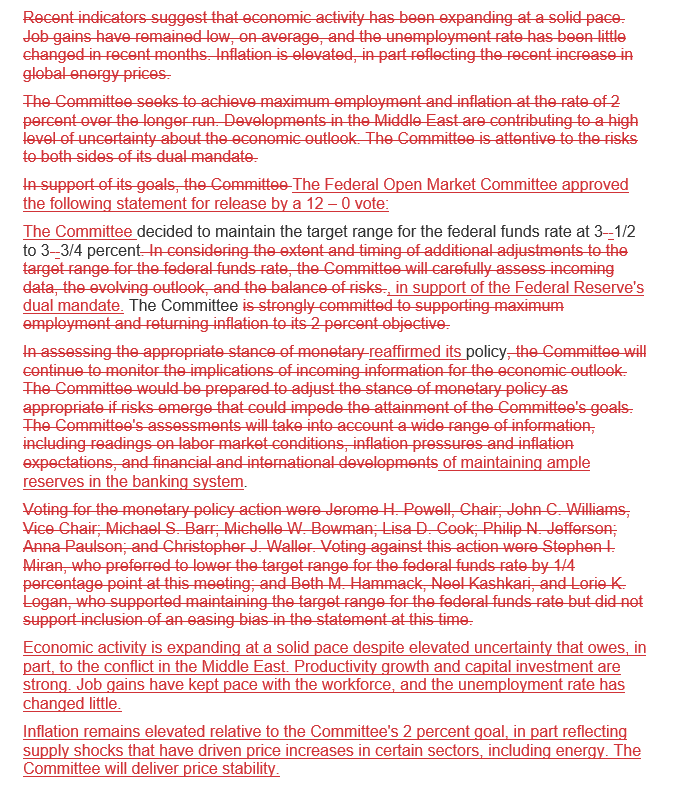

To begin with, even before the Warsh presser, in which he outlined the future of the “new” Fed, the markets were surprised by the modification to the FOMC statement.

The FOMC statement was only 114 words, a whopping 60% shorter than the previous statements.

There was no division (a positive surprise) as the Committee approved the statement by 12-0.

Furthermore, there is an unequivocal commitment to deliver price stability.

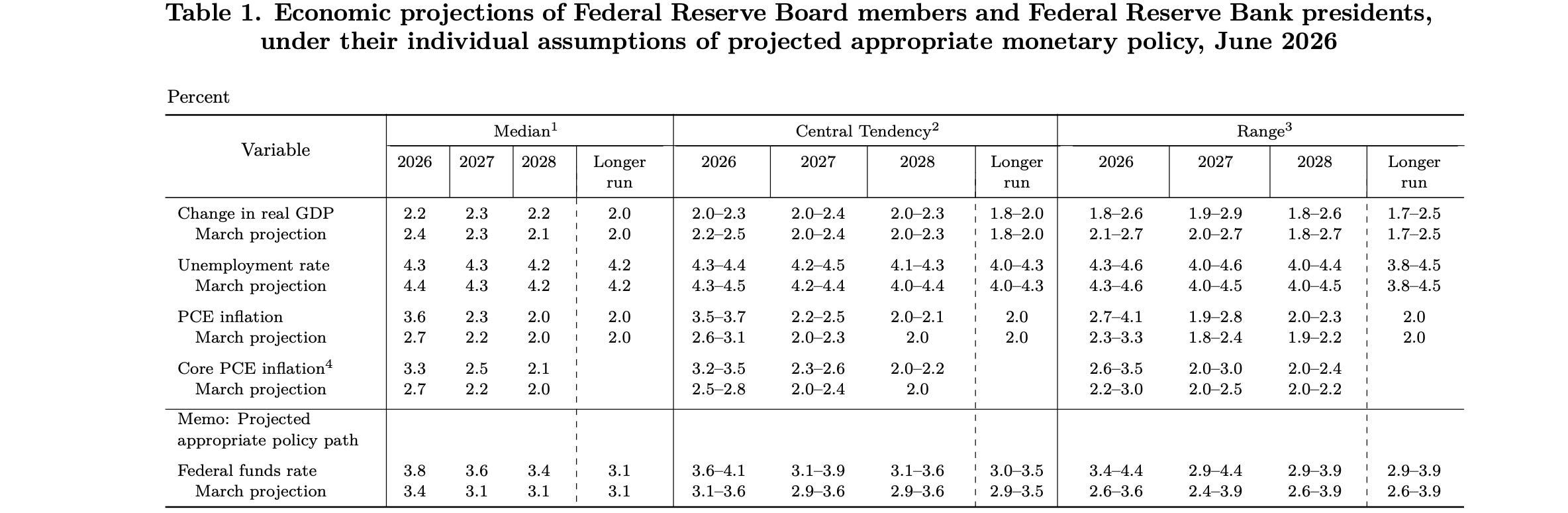

Warsh emphasised the 2% goal, which the Fed has failed to achieve since the COVID-led inflationary shock.

According to the dot plots, the Fed hopes to achieve the 2% goal only by 2028 (and we believe that only if there is no other black swan/geopolitical shock).

As the asset price inflation continues at an unprecedented pace, and frequent supply shocks rock the global economy, it’s challenging to achieve the 2% goal.

Interestingly, Warsh made a significant distinction about the restrictiveness of the monetary policy.

“And if I look at the housing markets as one example, Fed policy isn’t the single determinant of the state of the housing market, but broadly I would say there Fed policy appears to be somewhat restrictive.”

While he believes the policy is “somewhat” restrictive in the housing market, he takes the opposite view regarding the equity markets.

As someone who has been analysing macro data for a long time, we always watch out for trends in the data (long-time subscribers will concur with this view).

The Fed Chair mentioned the same, and according to him, the labour market is in a healthy position.

“Trends matter more than data points. What’s happening over three or six months matters more than any one data point, any one data release. And I’d say the jobs data has been moving in a good direction.”

Regime Change!

In Warsh’s own words:

What we’ve given markets is a new chapter for the central bank, some fresh thinking.

With 100% certainty, we can predict that the brain behind the Fed revamp is none other than Treasury Secretary Scott Bessent.

Bessent has openly expressed his views on the significant reforms needed at the Fed and has criticised its approach to managing inflation in recent years.

Thus, unsurprisingly, we got Warsh’s plan to revamp the Fed’s current structure.

“My Fed colleagues and I will be working in close collaboration to ask what changes might improve the conduct of monetary policy.”

Warsh has announced the formation of the following task force:

Fed communications.

Fed’s balance sheet policy.

Use and reliance on existing data sources

Productivity & jobs in an era of transformation.

Fed’s inflation framework.

In the last few years, JayPo used Nikkileaks to provide forward guidance, an unusual move for the Fed that, in some ways, reduced volatility and uncertainty.

However, with forward guidance now a thing of the past, markets (especially bond) will “more” violently react to macro data/ political statements (Trump).

Furthermore, the FOMC days will lead to extremely elevated volatility.

“But when all the financial markets are doing is reflecting back what we’ve said, then we’re taking the most important source of information and we’re being blind to it. I’d like us to create a system where those blinders come off, where markets are following data that they efficiently think is reliable.”

The “reliable” part is interesting and will lead to confusion in the early days until the task force releases the list.

Nevertheless, whenever the Fed adopts the task force recommendations, we will review the whole mechanism (market reaction, macro framework, etc.).

Since starting this newsletter, we have firmly believed that the primary problem with the Federal Reserve's monetary policy is its reliance on highly lagging data. Additionally, the transmission mechanism operates with a considerable lag, further complicating the process.

The dual mandate focuses on price stability and maximum employment, and the biggest data points, CPI and the Non-Farm Payrolls (NFP), are lagging data.

In fact, the first print of NFP is useless for half a year, with multiple monthly revisions and then annual revisions.

As a result, the Fed had been behind the curve, making historic mistakes, such as calling inflation “transitory” post-COVID.

Warsh has vowed to conduct monetary policy based on “real-time data”.

“As you know, there are normal long and variable lags in the conduct of monetary policy. What we’re really interested in is what’s happening right now. What we’re less interested in is echoes of history.”

While we appreciate the efforts, unless we receive a concrete framework for replacing the current data sources, forecasting the future is futile.

Warsh showed too much promise; however, only time will tell how much he can achieve.

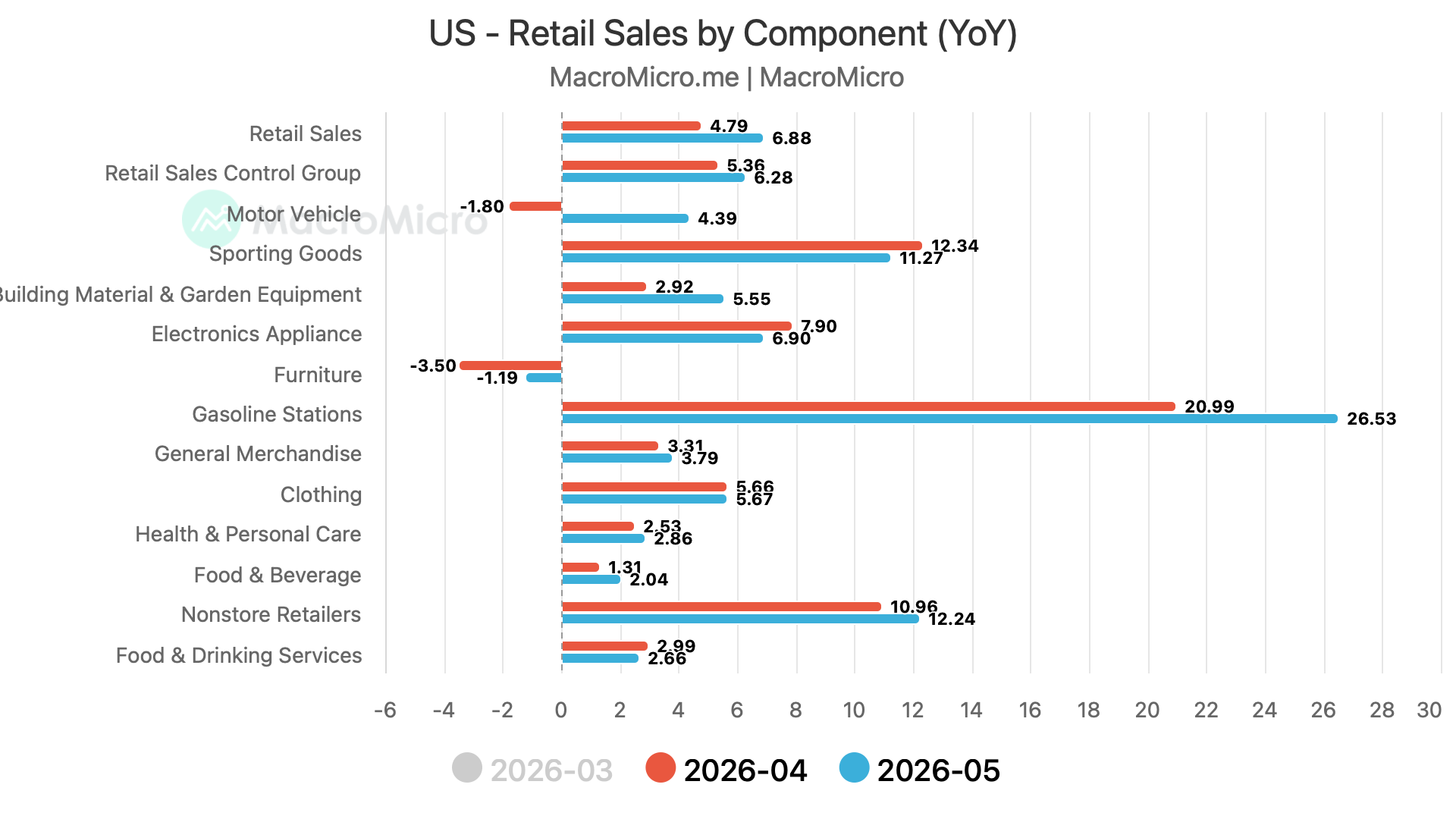

Retail sales was the biggest data point of this week.

Headline Retail Sales came in at 0.9% v/s Exp. 0.6%.

The Retail Sales ex Auto came in at 0.8% v/s Exp. 0.6% and the Retail Sales Control Group came in at 0.7% v/s Exp. 0.4%.

It was an all-around beat.

The strongest growth was in Nonstore Retailers, which rose by an astounding 12.24% (driven by inflation and higher nominal growth).

Furniture was the only category which registered degrowth, likely indicating the fragile housing market.

Equities!

Before we look at the technical charts, let us show you the two mind-blowing stats: